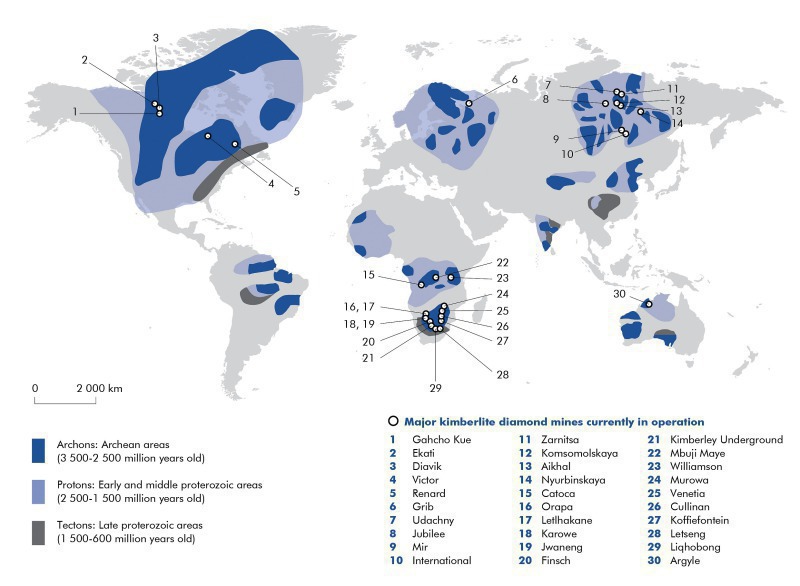

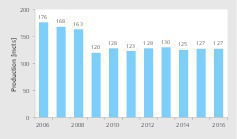

Production of rough diamonds

Current market and technology trends Quelle/Source: De Beers

Quelle/Source: De Beers

Quelle/Source: Petra Diamonds

Quelle/Source: Petra Diamonds

Quelle/Source: Alrosa

Quelle/Source: Alrosa

Quelle/Source: Bain & Company

Quelle/Source: Bain & Company

Quelle/Source: OneStone Research

Quelle/Source: OneStone Research

Quelle/Source: OneStone Research

Quelle/Source: OneStone Research

Quelle/Source: Alrosa

Quelle/Source: Alrosa

Quelle/Source: De Beers

Quelle/Source: De Beers

Quelle/Source: De Beers

Quelle/Source: De Beers

Quelle/Source: Rio Tinto

Quelle/Source: Rio Tinto

Quelle/Source: Dominion Diamond Corporation

Quelle/Source: Dominion Diamond Corporation

Quelle/Source: Dominion Diamond Corporation

Quelle/Source: Dominion Diamond Corporation

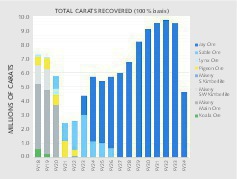

Quelle/Source: Petra Diamonds

Quelle/Source: Petra Diamonds

Quelle/Source: Lucura Diamond Corp.

Quelle/Source: Lucura Diamond Corp.

Quelle/Source: Lucura Diamond Corp.

Quelle/Source: Lucura Diamond Corp.

Quelle/Source: TOMRA Sorting Solutions

Quelle/Source: TOMRA Sorting Solutions

Quelle/Source: thyssenkrupp Industrial Solutions

Quelle/Source: thyssenkrupp Industrial Solutions

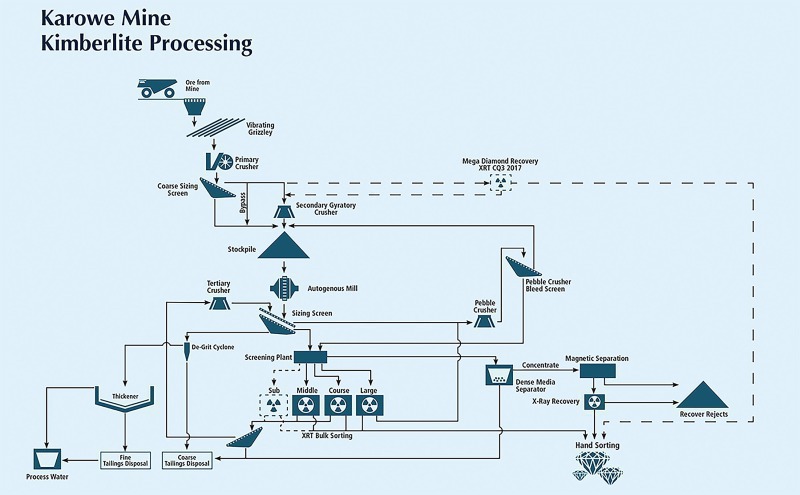

Quelle/Source: Stornoway

Quelle/Source: Stornoway

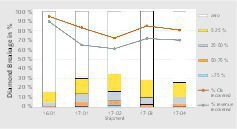

Quelle/Source: TOMRA Sorting Solutions

Quelle/Source: TOMRA Sorting Solutions

Summary: The production of rough diamonds already reached a peak value more than 10 years ago. Predictions see a continuation of the market downturn for mined diamonds up to 2030. Nevertheless, the medium- and long-term market outlook is good, especially in view of the rising prices and improved technologies. This article provides an insight into current market developments and explains important trends.

1 Introduction

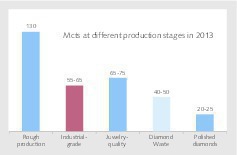

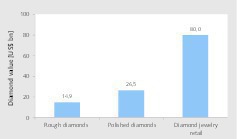

In 2016, the diamond jewelry sales market was at a level of US$ 80 billion while the market for industrial diamonds was US$ 25 billion. The volume relations, on the other hand, are significantly different. While only around 23 million carats (or 4.6 t) of cut and polished diamonds went into the jewelry market, some 16 billion carats or 3200 t of diamonds were produced for the industrial market. Only 12.5 t of the mined rough diamonds, i.e. less than 0.01 %, go into the production of industrial diamonds, 99.9 % of which are produced synthetically. In the meantime, the synthetic...